If this week felt disorienting, you were not imagining it. Markets delivered whiplash, but not because of a crash. What unfolded was far more structural. While headlines screamed about tech trouble, a quieter but historic shift took place beneath the surface.

Mega-cap technology stocks stumbled, dragging the NASDAQ lower, while value stocks, industrials, and small caps surged. Almost unnoticed in the noise, the Dow Jones Industrial Average crossed 50,000 for the first time in history — a psychological milestone that signals not fear, but reallocation.

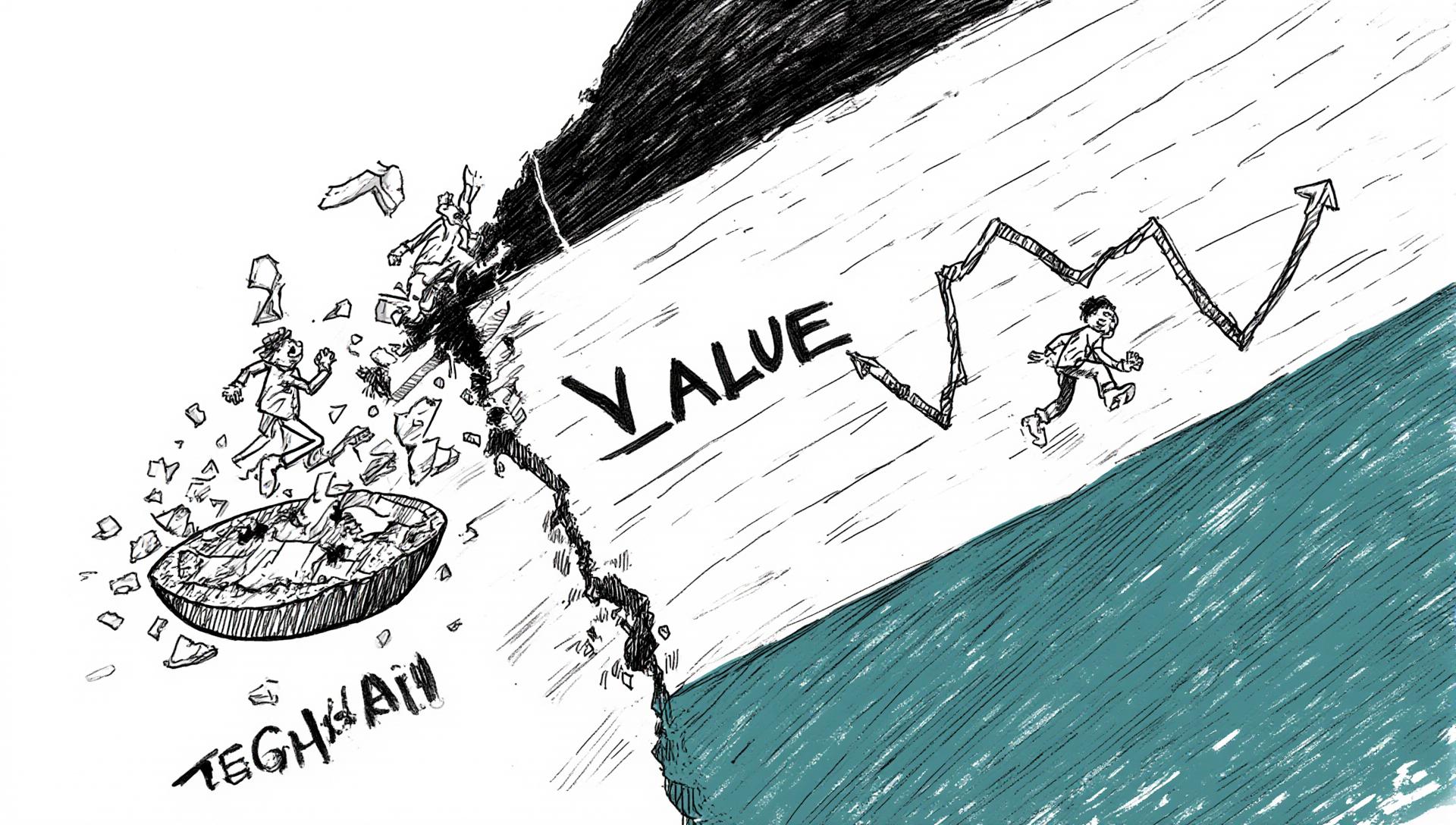

This was not a risk-off week. It was a rotation week. Capital did not flee equities; it simply changed destinations. Investors moved away from expensive promises of future growth and toward companies generating cash today.

Below is a structured breakdown of what mattered, what didn’t, and what could redefine market leadership in the days ahead.

United States: A Historic Rotation Takes Shape

At index level, the divergence was striking. The NASDAQ fell roughly 1.8 percent, weighed down by mega-cap technology. Meanwhile, the Dow rose 2.5 percent, powered by industrials, financials, and value stocks. Small caps extended their gains, reinforcing the message.

The spread between value and growth stocks reached nearly 400 basis points in a single week — an extraordinary move by professional standards. This was not gradual repositioning. It was decisive.

Investors are not abandoning equities. They are abandoning duration. High-growth technology stocks are priced on earnings far into the future. As capital expenditure requirements for AI infrastructure explode, investors are questioning whether returns will justify the cost.

This is not the end of the AI story. It is the end of unquestioned optimism. The market is reassessing how expensive growth has become.

Crucially, this rotation is happening alongside contradictory economic signals. Labor data is weakening sharply. ADP private payrolls showed just 22,000 new jobs in January. Job openings fell to their lowest level since 2020, and announced layoffs surged to the highest January total since 2009.

On its own, that data would suggest recession. Yet manufacturing told a very different story. The ISM Manufacturing Index jumped to 52.6, its strongest reading since 2022 and firmly back into expansion territory.

The synthesis is clear. The US economy is experiencing a white-collar slowdown and a blue-collar rebound simultaneously. Services and tech are retrenching, while goods production is accelerating after prolonged inventory depletion.

Markets are repricing growth — not collapsing, but changing leadership.

Europe: The Quiet Beneficiary of Rotation

While US investors debated tech valuations, Europe quietly advanced. The STOXX Europe 600 reached new highs, rising about 1 percent for the week. France’s CAC 40 gained nearly 2 percent.

The primary driver was inflation — or rather, the lack of it. Eurozone CPI slowed to 1.7 percent year over year in January, undershooting the European Central Bank’s target. That gives policymakers flexibility and reassures investors that rate cuts can proceed without reigniting price pressures.

The ECB held its deposit rate at 2.0 percent and emphasized resilience. Growth remains modest, but stability is improving. Retail volumes dipped in December, yet the broader fourth-quarter trend was firmer than mid-2025.

Europe’s rally is investment-led, not consumption-driven. It reflects confidence in policy optionality rather than a spending boom. The consumer is holding up, but cautiously — “fine with an asterisk.”

United Kingdom: One Vote Away From a Cut

The FTSE 100 gained 1.4 percent, but the real drama unfolded inside the Bank of England. The policy decision ended in a razor-thin 5–4 vote to hold rates at 3.75 percent.

Four members voted for an immediate cut. That split signals a profound shift in internal sentiment. The UK is now one data print away from a rate-cutting cycle.

Markets are watching closely. With officials suggesting inflation may return to target sooner than expected, expectations are building for a possible move as early as March.

For households under pressure from resetting mortgage rates, relief may be close — but not yet guaranteed.

Japan: Election Optimism, Currency Warning

Japanese equities rallied ahead of the February 8 lower-house election. The Nikkei rose 1.75 percent, while the broader Topix surged nearly 4 percent.

Markets are pricing in fiscal expansion. Expectations of increased government spending have lifted equities, but the currency told a more cautious story. The yen weakened toward 157 per dollar, reflecting concerns over debt issuance and monetary dilution.

Households are not sharing the optimism. December household spending fell 2.6 percent year over year. Inflation driven by a weak currency is eroding purchasing power.

Japan’s market is celebrating stimulus expectations, while consumers tighten belts. That disconnect will eventually need to resolve.

China: Uneven Recovery, Uneasy Markets

Chinese equities slipped, with the CSI 300 down 1.3 percent. Economic signals remain split.

Private-sector PMI data showed improvement, driven largely by exports. In contrast, official surveys highlighted weak domestic demand. Chinese firms selling abroad are coping. Firms reliant on local consumers are not.

Markets continue to wait for policy support. For now, expectations are doing the heavy lifting, while consumption remains hesitant.

The Week Ahead: February 9–13

Next week delivers a dense and potentially market-defining data calendar.

Tuesday brings US retail sales, testing whether consumers are pulling back as labor data suggests. Wednesday is pivotal: China’s inflation data and the delayed US jobs report arrive together, clarifying whether labor weakness is real or overstated.

Thursday delivers UK GDP, a potential tiebreaker after the Bank of England’s split vote. Friday closes with the delayed US CPI — the ultimate volatility trigger.

This is not a week for complacency.

Top Five Risks to Watch

US jobs report whiplash

A weak print validates slowdown fears; a strong print reprices rate-cut expectations instantly.

US CPI surprise

Hot inflation pressures long-duration assets further; cooler data accelerates the rotation.

Tech capitulation versus rebound

Another leg down drags indices; a rebound reignites concentration risk.

UK GDP shock

Weak data pulls forward cuts and weakens sterling; strong data delays relief.

China inflation signal

Soft data revives stimulus hopes; firmer inflation complicates policy response.

Final Insight: A Structural Test Begins

This week felt like a changing of the guard. The Dow crossed 50,000 as technology stumbled, but the deeper question is whether this new leadership can carry the market.

For years, a handful of mega-cap tech stocks powered index returns. If that engine stalls, can banks, industrials, and value stocks provide enough momentum?

Next week is not just about data releases. It is a structural stress test. The market is trying to stand on new legs — and we are about to find out how strong they really are.

FAQs

Is this a market crash?

No. Capital is rotating within equities, not exiting them.

Is the AI story over?

No, but valuations are being challenged by rising costs and return uncertainty.

Why are value stocks outperforming now?

They offer near-term cash flows and lower sensitivity to rates.

Why does US labor data matter so much?

It anchors the soft-landing narrative and Fed expectations.

What matters most next week?

US jobs and CPI — together they will set the tone.

Hashtags

#WeeklyMarketUpdate #MarketRotation #ValueStocks #TechStocks #Dow50000 #GlobalMarkets #Inflation #EconomicOutlook #InvestmentStrategy #MarketVolatility

Subscribe to our Newsletter

Discover more