This holiday-shortened week delivered one of the most dramatic narrative shifts of 2026.

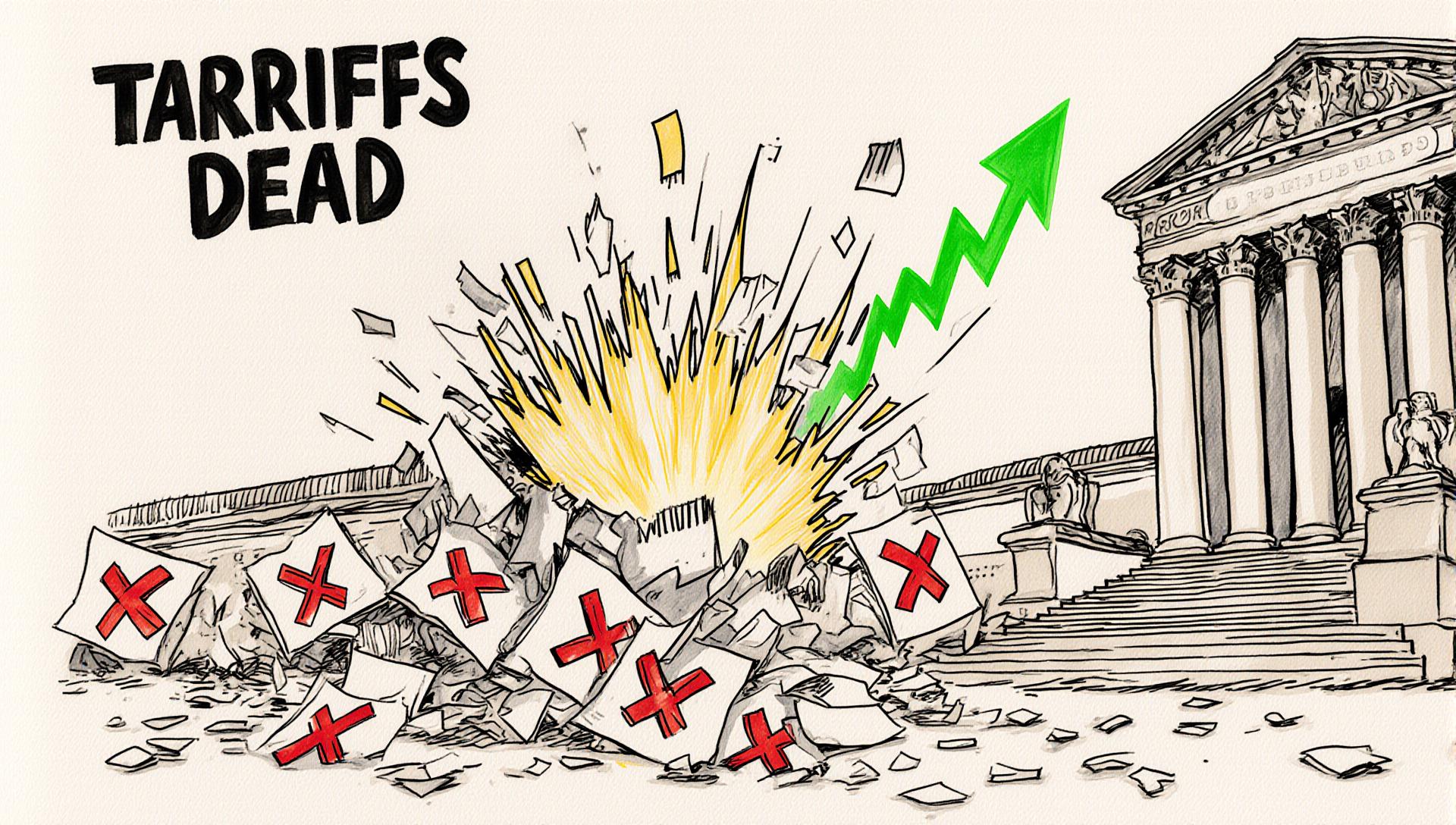

The US Supreme Court overturned the previous administration’s global tariffs in a 6–3 ruling, effectively dismantling a major pillar of trade policy that had shaped corporate strategy for years. Markets celebrated instantly. The S&P 500 jumped 1.1 percent. The NASDAQ rose 1.5 percent. Losing streaks snapped.

But beneath the relief rally lies a far more complicated story.

While the legal framework for global trade just improved overnight, US growth slowed sharply and inflation reaccelerated. The result is a split-screen reality: a structural policy win colliding with deteriorating macro momentum.

Below is your structured breakdown of what mattered — and what could reshape positioning next week.

United States: Legal Clarity, Economic Tension

The Supreme Court ruling removed a major source of friction from global commerce.

Tariffs functioned as taxes on imports, supply chains, and corporate earnings visibility. By declaring that the administration exceeded its legal authority, the Court eliminated the executive unpredictability that had clouded trade relations for years. Markets immediately repriced global trade risk lower.

There is also a second layer still unfolding: the refund question.

If the tariffs were illegal from inception, companies may be entitled to recover billions in previously paid duties. The administrative process would be complex and slow, but the possibility of windfall reimbursements strengthened corporate balance sheet expectations.

However, the macro data delivered a cold counterweight.

Fourth-quarter GDP slowed sharply to 1.4 percent annualized, down from 4.4 percent in Q3. While part of the deceleration reflects shutdown-related distortions, private-sector momentum clearly softened. Consumer spending is holding up, but investment is pausing.

More troubling was inflation.

Core PCE — the Federal Reserve’s preferred gauge — rose 0.4 percent month-over-month and now sits at 3.0 percent year-over-year. Headline PCE reached 2.9 percent, its highest reading since March 2024. The clean disinflation narrative is no longer intact.

This creates a policy dilemma.

The January Fed minutes revealed division within the committee. Some members see slowing growth and argue for easing. Others view persistent inflation as justification for maintaining restrictive policy. The ingredients of stagflation — cooling growth and sticky prices — are visible, though unemployment remains relatively stable for now.

Adding to the pressure, oil prices rose 6 percent this week amid escalating US–Iran tensions. WTI crude moved above $66 per barrel. Energy costs represent the fastest transmission mechanism into consumer inflation and could quickly worsen growth dynamics if sustained.

The legal environment improved. The economic environment deteriorated.

Europe: Sentiment Leading, Data Lagging

European equities outperformed, with the STOXX 600 rising more than 2 percent. The rally reflects relative valuation appeal and capital rotation out of US tech-heavy indices.

However, the data remains mixed.

Eurozone industrial production fell 1.4 percent in December, significantly worse than expected. Germany’s manufacturing sector continues to struggle. Yet business sentiment surveys tell a different story. The PMI for new orders rose at the fastest pace in four years.

This gap between sentiment and production is crucial. Markets are betting that improving confidence is a leading indicator and that industrial weakness is lagging.

Complicating matters, speculation emerged regarding ECB leadership. Reports circulated suggesting Christine Lagarde could step down early, though she reaffirmed her intention to complete her term. Even so, succession jockeying has reportedly begun, with southern European blocs positioning themselves.

Markets currently ignore the governance risk. But central bank uncertainty rarely stays dormant.

United Kingdom: Weakness Signals Easing

The FTSE 100 rose 2.2 percent, reaching new peaks.

The rally is driven by expectations of policy relief rather than economic strength. Unemployment climbed to 5.2 percent — a five-year high. Wage growth is slowing. The labor market is visibly deteriorating under high interest rates.

For traders, this implies the Bank of England pivot is near.

Inflation cooled to 3.0 percent, supporting the case for easing. Markets are increasingly pricing in a March rate cut. This is classic “bad news is good news” behavior: weaker employment increases the probability of liquidity support.

The risk, however, is external. Rising global oil prices could complicate the inflation outlook and delay that pivot.

Japan: Growth Stall and Policy Questions

Japan underperformed modestly, with the Nikkei drifting lower.

Fourth-quarter GDP came in at just 0.2 percent annualized, far below expectations of 1.6 percent. Private consumption was essentially flat at 0.1 percent growth. Domestic demand remains fragile.

The yen weakened toward 154 per dollar. Typically, currency depreciation supports exporters and lifts equities. This time, growth concerns overshadowed currency benefits.

Inflation slowed to 2.0 percent, its lowest pace in two years, raising concerns that Japan may slide back into its familiar low-growth, low-inflation equilibrium.

Prime Minister Taichi has called for proactive fiscal policy, but concrete action has yet to materialize. Japan’s economy currently lacks visible momentum.

China: Policy Confusion and Reopening Risk

With mainland markets closed for Lunar New Year, trading was limited — but headlines were not.

The US Pentagon briefly released — and then withdrew — a list of companies allegedly tied to military support, including major names such as Alibaba and BYD. Even though the list was retracted, the reputational damage and risk premium implications remain.

You cannot unring that bell.

Meanwhile, the IMF projected 4.5 percent Chinese growth for 2026 and emphasized the need to pivot toward consumption-led expansion. Domestically, China raised telecom VAT from 6 to 9 percent, directly impacting profitability in that sector.

When mainland markets reopen Tuesday, investors will confront a week’s worth of geopolitical uncertainty and tax policy adjustments simultaneously.

The Week Ahead: February 23–27

Tuesday brings key US data, including consumer confidence and the Case-Shiller home price index. Confidence is critical given slowing GDP.

Friday delivers PPI. After a hot PCE print, pipeline inflation will be scrutinized closely.

In Europe, flash CPI readings for France and Germany will set the tone for ECB policy expectations.

In China, Tuesday’s market reopening could generate volatility as investors process geopolitical headlines.

Top Five Risks to Watch

US inflation repricing

If PPI reinforces inflation persistence, markets may price out rate cuts and tighten financial conditions abruptly.

US consumer confidence deterioration

With GDP slowing, weakening confidence could shift the narrative toward recession risk.

Housing market vulnerability

Higher-for-longer rates could begin pressuring property valuations and banking sentiment.

European inflation surprise

Sticky CPI in France or Germany would undermine rate-cut expectations and challenge the European equity rally.

China reopening volatility

Geopolitical headlines and VAT changes could trigger sharp repricing in Chinese equities and spill over into broader Asian markets.

Final Insight: Sugar Rush or Structural Shift?

The Supreme Court delivered a major policy victory for global trade.

But legal clarity cannot offset a slowing economy and reheating inflation.

This week’s rally reflects relief. Next week’s data will determine durability.

If inflation persists while growth fades, markets face renewed tension between optimism and reality. The lawyers provided a win. The macro data issued a warning.

Watch the confidence numbers. Watch inflation. And watch whether this rally rests on fundamentals — or reflex.

FAQs

Why did markets rally so strongly?

Because the Supreme Court removed tariff uncertainty, reducing trade friction and corporate risk premiums.

Is the GDP slowdown temporary?

Shutdown effects contributed, but private-sector momentum is clearly softening.

Why is inflation rising again?

Service-sector costs, wages, housing, and energy remain sticky, preventing smooth disinflation.

Why is Europe outperforming?

Relative valuation appeal and improving sentiment surveys are driving capital rotation.

What matters most next week?

US consumer confidence and PPI, plus European inflation data and China’s reopening reaction.

Hashtags

#WeeklyMarketUpdate #GlobalMarkets #SupremeCourt #TradePolicy #Inflation #FederalReserve #GDP #EnergyMarkets #ChinaMarkets #EuropeanEquities #InvestmentStrategy #MarketVolatility

Subscribe to our Newsletter

Discover more